At a time when the world economy is contracting at Great Depression rates, you wouldn’t think that policy makers would be worried about inflation.

Category: Fiscal Policy

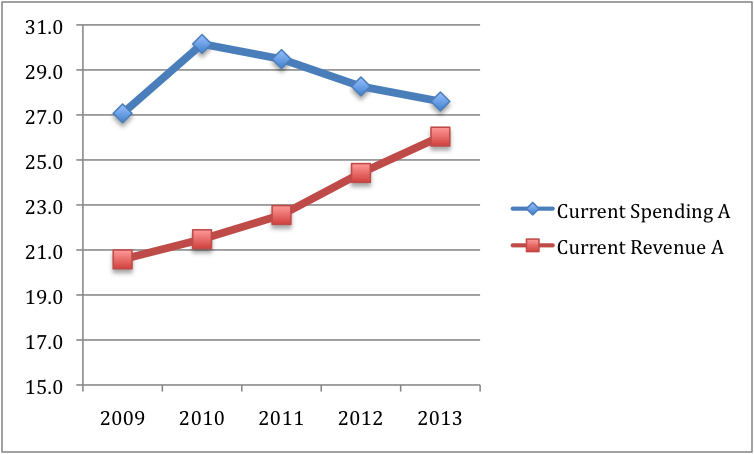

Much of the post-budget analysis has focused on whether the correct balance between taxation and spending measures has been achieved. In fact, the 5 year plan leaves this quite open, at least in terms of the ultimate convergence towards the 3 percent budget target in 2013. This is because the plan leaves unallocated €4 billion in 2012 and €7 billion in 2013.

In the two charts below, I show the polar alternatives: in the first chart, all of the allocation is to higher taxes in 2012 and 2013; in the second chart, all the adjustment is to lower spending in 2012 and 2013. (Fiscal variables are expressed as ratios to GDP.)

The economic debate at the next general election may well focus on the relative merits of the two adjustment paths. [Of course, the likely outcome is an interior solution.]

While there is a lot of detail to absorb and plenty of issues to debate, internal consistency demands that I welcome the Minister’s budget deficit target for this year of 10.75%. I argued a few weeks ago that when considering whether the government was sticking to the plan it had sent to Brussels in January, it was best not to focus on the target of a 9.5% budget deficit for the year as a whole but on whether the measures taken would, if implemented over a whole year, put us on a 9.5% pace. Based on current information, I think the budget does this.

Last week’s Exchequer Returns indicated that we were on path of a deficit of 12.75% this year without further corrective action. On a full-year basis, this would require an adjustment of 3.25% to get to a 9.5% deficit. Assuming that the corrective actions taken in this budget would have only 60% of their full year effect during 2009, then these measures would reduce this year’s deficit by (0.6)(3.25)% = 1.95%, which would imply a budget deficit for 2009 of 10.8%. As such, I would interpret the government’s actions today as putting them back on track with the plan sent to Brussels in January.

Another welcome element of the budgetary figures was that the GDP projection of -8% were more realistic than the -6.75% mentioned in last week’s Exchequer Returns. Both the QNAs and the recent unemployment data point towards a GDP decline for this year of at least the 8% now projected by the government.

I’m still reading over the governments plans for the banks and will post my thoughts later.

Update: I should probably have also pointed out that it is perhaps a bit disappointing that the targets for 2010-2012 have slipped a bit since January. But then again, these relatively small adjustments should be seen as realistic in the face of the govenment’s projections of -8% and -3% GDP growth for 2009 and 2010, compared with projections of -4.5% and -1.1% in January.

I am opening this thread in order to facilitate those who wish to comment on the budget.

As signalled by Eurointelligence, the FT carries this story today about how Germany is creating new products to target retail investors for its sovereign debt.