If you would like to participate in the online survey that feeds into the compilation of the World Economic Forum’s Global Competitiveness Report, please email ncc at forfas.ie

Month: April 2009

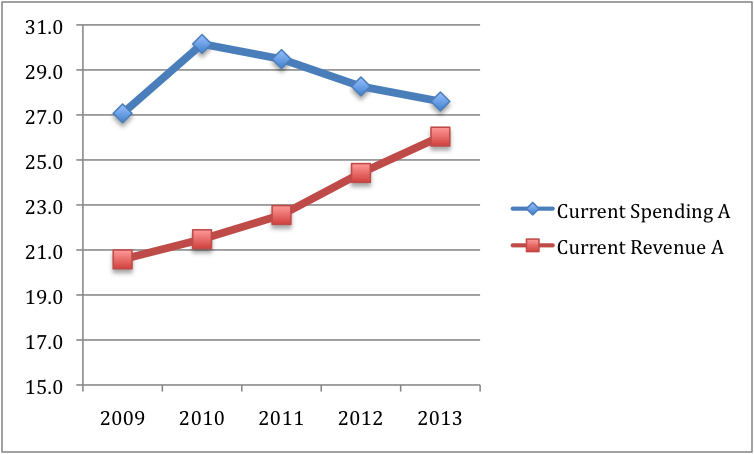

Much of the post-budget analysis has focused on whether the correct balance between taxation and spending measures has been achieved. In fact, the 5 year plan leaves this quite open, at least in terms of the ultimate convergence towards the 3 percent budget target in 2013. This is because the plan leaves unallocated €4 billion in 2012 and €7 billion in 2013.

In the two charts below, I show the polar alternatives: in the first chart, all of the allocation is to higher taxes in 2012 and 2013; in the second chart, all the adjustment is to lower spending in 2012 and 2013. (Fiscal variables are expressed as ratios to GDP.)

The economic debate at the next general election may well focus on the relative merits of the two adjustment paths. [Of course, the likely outcome is an interior solution.]

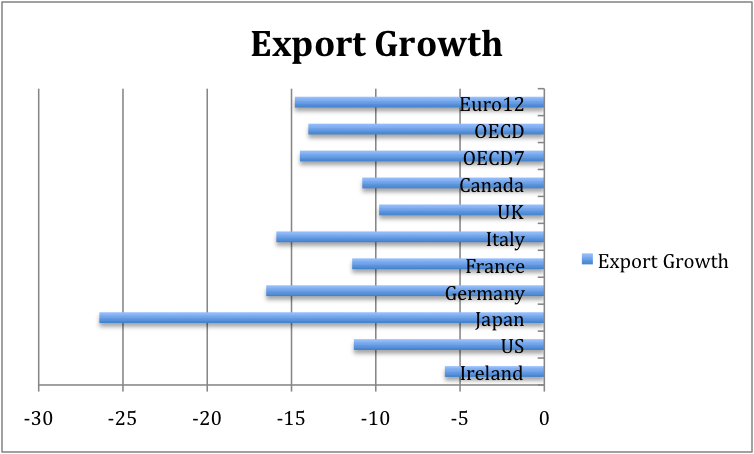

The Irish economy is undergoing a very large contraction this year. The major source of the decline is the contraction in domestically-orientated activities. It is true that exports are also falling – but it is important to put that into a global context. The graph below shows projected export growth for 2009 for a range of countries (OECD projections, except Ireland where it is last week’s Central Bank forecast). In a cross-country comparative context, the global trade shock is bigger for many other countries. (However, a given decline in export growth has a bigger impact here than in many of these countries, in view of our high export share in output.) One reason is that we do not produce the types of durables and capital goods that have taken the biggest hit in terms of cancelled orders and so on.

My previous post discussed the price that our new National Asset Management Agency (NAMA) could pay for impaired loans from the perspective of how much of a loss relative to book value the banks could take under the assumption that the government didn’t invest more than its €7 billion planned re-capitalisation. The answer was that the discount from book value would have to pretty small relative to the figures being widely quoted for likely losses.

Admittedly, this was a bit of an around-the-houses way of warming up to the NAMA discussion and Patrick was completely correct in his comment that the key sentence in the speech was

If the crystallisation of losses at any institution requires additional capital the State will insist on participation by way of ordinary shares in the relevant institution.