| 26-07-2012 | NTMA Announces Bond Switch and Outright Sale. |

|

| 26-07-2012 | Offering Circular for new 5.50% Treasury Bond 18 October 2017. |

Month: July 2012

Since Brendan and Philip have both posted on competitiveness in the past couple of days, I thought I’d follow up with a link to the following piece by Gaulier, Taglioni and Vicard.

Eurointelligence points us to a piece by Alan Beattie on the political difficulties which the IMF faces in dealing with the Eurozone crisis. As we know in Ireland all too well, while the IMF has generally been on the side of the angels, it is the ECB and EC that have called the shots, with the result that the IMF’s reputation suffers by association with Troika policies that are a complete and utter disaster. The dilemma for the IMF is that a complete withdrawal from the Eurozone crisis, while the single currency collapses, won’t do its reputation much good either.

Charles Goodhart and Sony Kapoor have it right, I think: it is the Eurozone that is dysfunctional, and in the future IMF conditionality has to be directed at the ECB and other Eurozone-level bodies as much as (if not more than) it is directed at individual member states. It’s time for the IMF to decide whether it wants to prove Peter Doyle right, or prove him wrong.

Brendan Walsh highlights the importance of the external value of the euro for competitiveness. In fact, recent IMF work (not yet online) shows it is very important for all peripheral countries (even though cross-border finance is primarily obtained within the euro area, cross-border trade is much more extensive).

Martin Feldstein has a new FT op-ed also on the importance of a weaker euro here.

The role of the depreciation of the euro against the dollar during 1999-2001 in creating divergences within the euro area is analysed in this paper I co-authored with Patrick Honohan.

The orthodox view is that enhanced competitiveness should play a significant part in Ireland’s (and other euro area countries’) recovery from recession.

In the March 2012 “Review Under the Extended Arrangement” the IMF team states that:

“Ireland’s economy has shown a capacity for export-led growth, aided by significant progress in unwinding past competitiveness losses.” (my italics)

The evidence does indeed point to a significant improvement in Ireland’s competitiveness between 2008 and the present. The following two graphs show the ECB’s ‘Harmonized Competitiveness Indicator’ (HCI) based on (a) Consumer Prices and (b) Unit Labour Costs. (A rising index implies a loss of competitiveness.) Both graphs show a competitive gain since 2008, with second showing the more dramatic improvement. However, this measure is affected by the changing composition of the labour force, which became smaller but more high-tech as a result of the collapse of many low-productivity sectors during the recession.

Concentrating on the HCI based on the CPI, the Irish competitive gain has still been impressive – our HCI fell 17% between mid-2008 and mid-2012, giving us the largest competitive gain recorded in any of the 17 euro-area countries over these years. Greece, at the other extreme, recorded no change in its HCI, Portugal fell only 4.5%, Spain 6.6%, Italy 6.8%. So by this measure Ireland is some PIIG(S)!

However, we need to dig deeper and understand why Ireland’s HCI has fallen so steeply.

Part of the story – the part on which some commentators dwell – is that early in the recession the Irish price level and Irish nominal wages fell. From a peak of 108 in 2008 the Irish Consumer Price Index fell to 100 in January 2010. But it has started to rise again – by mid-2012 it was back up to 105. The fall in the Harmonized Index of Consumer Prices has been even less impressive – from a peak of 110 to a low of 105 and now rising back to its previous peak.

Wages are more important than prices as an index of competitiveness because price indices are influenced by indirect taxes and include many non-traded services and administered prices. But Irish nominal wages tell much the same story as the price indices. The index of hourly earnings in manufacturing peaked around 106 at the end of 2009 (2008 = 100) and then fell to a low of 102 in 2011, where it appears to have stabilized. Even in the construction sector, where employment collapsed in the wake of the building bust, wage rates declined only 6 per cent between 2008 and 2011.

Falling wages and prices are in line with what many commentators thought would happen after the surge in unemployment in 2008. Widely-publicized wage cuts in the private and public sectors were seen as part of the ‘internal devaluation’ needed to rescue the Irish economy from the recession. It was argued that this was the only way we could engineer a reduction in our real exchange rate given our commitment to the euro. (Paul Krugman likes to refer pejoratively to an ‘internal devaluation’ as simply ‘wage cuts’.)

However, the Irish wage and price deflation has not been very dramatic and seems to have stalled in 2011, even though the unemployment rate continues to climb.

So why has Ireland’s competitiveness improved so sharply since 2008 if the ‘internal devaluation’ has been so modest? The answer, of course, lies in the behaviour of the euro on world currency markets and the fact that non-euro area trade is much more important for Ireland than for any other member of the EMU.

This can be seen by looking at the HCI for the euro area as a whole. The euro area HCI fell from 100 in mid-2008 to 84.7 in mid-2012 – almost as big a fall as was recorded for Ireland and far higher than that recorded in any other euro area country.

The paradox that the euro area HCI has fallen much further than the average (however weighted) of the constituent EMU countries is explained by the fact that for each individual country the HCI is compiled using weights that reflect the structure of that country’s total international trade, but for the euro area as a whole the weights reflect the only the area’s trade with the non-euro world.

In its notes on the series the ECB draws attention to this:

“The purpose of harmonized competitiveness indicators (HCIs) is to provide consistent and comparable measures of euro area countries’ price and cost competitiveness that are also consistent with the real effective exchange rates (EERs) of the euro. The HCIs are constructed using the same methodology and data sources that are used for the euro EERs. While the HCI of a specific country takes into account both intra and extra-euro area trade, however, the euro EERs are based on extra-euro area trade only.” (my italics)

It is understandable that Ireland should show a large competitive gain by euro area standards as the euro declined on world markets after 2008 because non-euro area trade is far more important to Ireland than to any of the other 16 members of the EMU. A fall in the dollar value of the euro does nothing to make France more competitive relative to Germany, or Greece relative to either of them, but it does a lot for Ireland relative to its two most important trading partners – the UK and the US.

As a consequence, the decline in the value of the euro on world currency markets, and especially relative to sterling and the dollar, has had a much larger effect on our competitiveness than on that of any other euro area country.

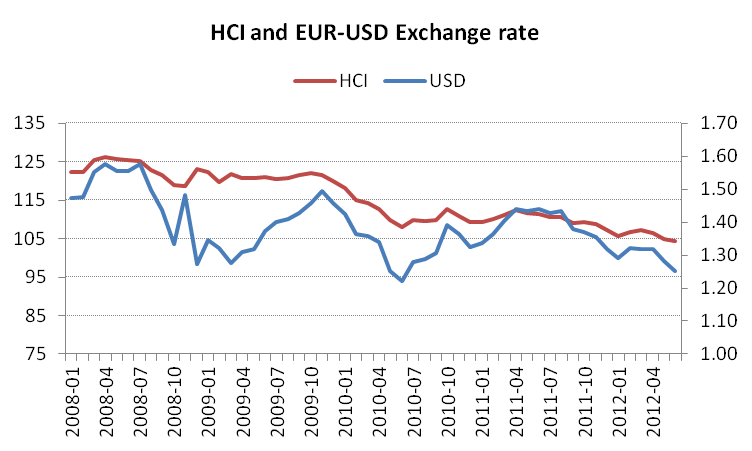

The following graph shows the USD / EUR exchange rate and Ireland’s HCI since 2008. It does not take any econometrics to convince me that the main driving force behind Ireland’s competitive gain has been the weakness of the euro. Undoubtedly a more sophisticated treatment, including the euro-sterling and other exchange rates of importance to Ireland – duly weighted – would show an even closer co-movement.

This should alert us to the point that Ireland’s much-praised recent competitive gain has been due more to the weakening of the euro on the world currency markets than to domestic wage and price discipline.

No doubt it could also be shown that a significant amount of the loss of competitiveness in the years before 2008 was due to the strength of the euro.

The fault – and the blame – lay not with us but with the far-from-optimal currency arrangement under which we labour.

Continuing gains in competitiveness would therefore seem to depend more on further euro weakness than on the process of ‘internal devaluation’. Should this have been a condition of our Agreement with the Troika?